Munich Re just partnered with ICEYE to embed synthetic aperture radar (SAR) flood observations directly into its Location Risk Intelligence platform. That is not a press release you skim and forget. It signals a structural shift in how the insurance industry measures, prices, and responds to flood risk.

For years, flood models have relied on historical return periods, elevation data, and hydrological simulations. Those tools still matter. But they share a fundamental limitation: they estimate what water might do. SAR satellites show what water actually did, within hours, regardless of cloud cover or daylight. When a USD 52.2 billion flood insurance market (projected by 2034 at a 15.2% CAGR) is built on models that struggle with real-time validation, the arrival of observation-based intelligence is not incremental. It is foundational.

Why SAR changes the equation

Synthetic aperture radar operates at C-band or X-band frequencies that penetrate clouds, rain, and smoke. Unlike optical satellites that need clear skies (a cruel irony during flood events), SAR captures surface water extent in near-real-time.

ICEYE’s constellation now delivers flood footprint data with sub-day revisit times over affected areas. That means:

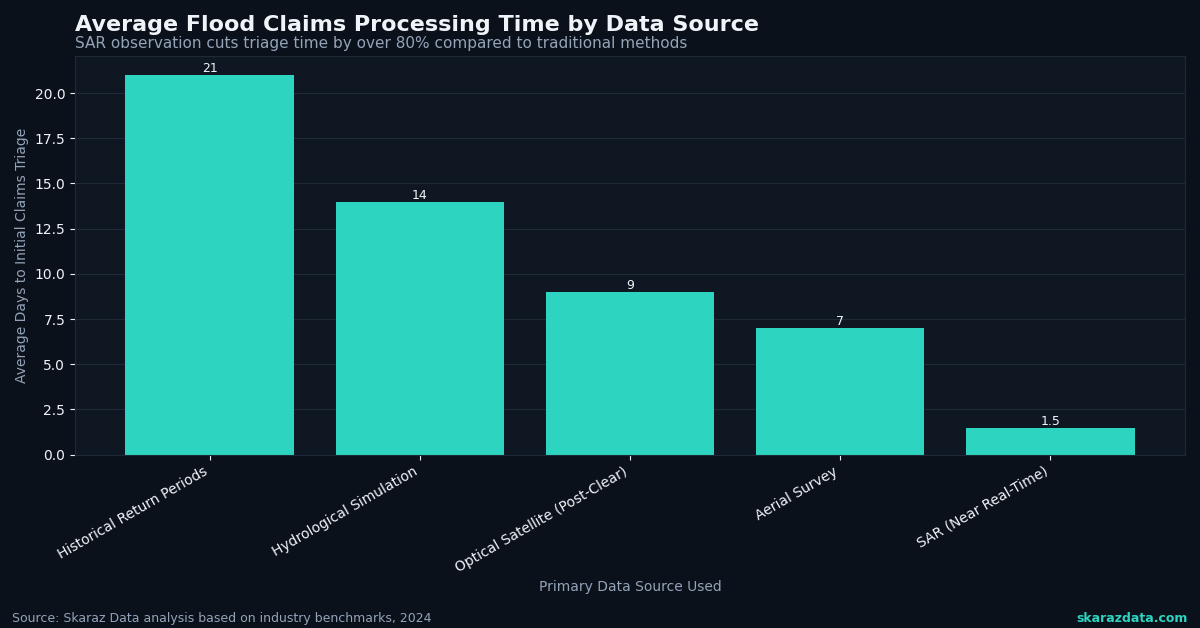

- Claims triage within 24 hours of a flood event, not weeks

- Portfolio-level exposure snapshots that show which policies are inside the actual inundation boundary

- Model validation loops where observed flood extents feed back into probabilistic models, correcting systematic biases in return-period estimates

Munich Re’s integration of this data into Location Risk Intelligence is the clearest signal yet that tier-one reinsurers consider SAR-derived flood intelligence production-ready.

The protection gap problem, quantified

AXA and Planet recently co-authored a piece on how space technology can close the insurance protection gap. The numbers behind that gap are stark. Globally, only about 30% of catastrophe losses are insured. For flood specifically, the ratio is often worse, particularly in emerging markets.

Consider the shrimp aquaculture sector in India, where recent research in Frontiers examines insurance strategies for an industry contributing to a USD 171 billion annual seafood trade. Flood and cyclone risk is existential for coastal aquaculture, yet parametric and indemnity products remain scarce because historical loss data is thin and unreliable.

SAR-based flood observations solve a core piece of this puzzle. When you can objectively measure inundation depth and duration from space, you unlock:

- Parametric triggers tied to observed water levels rather than weather station proxies

- Basis risk reduction because the measurement matches the actual peril, not a correlated index

- Scalable underwriting in data-sparse regions where ground-truth infrastructure does not exist

From Katrina’s legacy to modern portfolio intelligence

Hurricane Katrina generated USD 104.5 billion in insured losses twenty years ago. The insurance industry rebuilt its catastrophe modeling infrastructure in response, investing heavily in probabilistic hurricane and flood models. That generation of tools was a massive leap forward.

But the climate is not static. Moody’s 2025 emerging risk report highlights that compounding hazards (flood following wildfire, urban heat amplifying storm surge impacts, infrastructure interdependencies) are creating loss patterns that single-peril models struggle to capture.

Satellite observation layers add a calibration mechanism that keeps models honest. When your cat model predicts a 1-in-100-year flood footprint, and SAR data from five recent events consistently shows water reaching areas the model classifies as dry, you have an actionable signal to re-rate.

The property intelligence space is moving in the same direction. Aerial imagery (drones, aircraft, satellites) is becoming the backbone of property assessment, with insurers layering multiple data sources to build richer risk profiles. SAR flood data slots directly into this stack.

What a modern flood risk pipeline looks like

For technical leaders evaluating how to integrate satellite-derived flood intelligence, here is a practical architecture:

- Ingestion layer: SAR flood footprints (ICEYE, Copernicus Sentinel-1) delivered as GeoTIFF or vector polygons via API or cloud-native formats (COG, GeoParquet)

- Geocoding and matching: Spatial join against policy location data, using H3 hexagonal indexing or PostGIS for scalable point-in-polygon queries

- Exposure aggregation: Real-time portfolio dashboards showing affected sum insured, policy count, and treaty-level accumulation

- Model feedback loop: Observed flood extents compared against modeled return periods, with systematic bias metrics tracked over time

- Claims acceleration: Automated first-notice-of-loss enrichment, attaching flood depth estimates to individual claims before adjuster deployment

The key engineering consideration: SAR data volumes are large (a single Sentinel-1 scene is roughly 1 GB), and flood events generate bursts of data that need processing within hours. Cloud-native geospatial tooling (STAC catalogs, Dask/Xarray for raster processing, DuckDB for analytical queries) is essential for keeping latency acceptable.

The wildfire parallel

WIPO’s recent Green Technology Book documents how AI-powered satellites and thermal drones are transforming wildfire detection and management. The pattern is identical to what is happening in flood: space-based observation moves from research curiosity to operational intelligence, then insurers integrate it into underwriting and claims workflows.

The AI Journal’s coverage of technology in Indian home insurance underscores the same trend from the demand side. As natural catastrophe frequency increases, insurers who rely solely on historical models face adverse selection. Those who layer in real-time observational data can price more accurately and respond faster.

Where this is heading

The convergence is clear. SAR satellite constellations are reaching the revisit cadence needed for operational insurance use. Cloud-native geospatial infrastructure makes processing feasible at portfolio scale. And the market (at 15.2% CAGR) is large enough to justify the investment.

Insurers and reinsurers who build satellite-derived flood intelligence into their risk pipelines now will have a compounding advantage: better pricing accuracy, faster claims resolution, and the ability to underwrite in markets where traditional data is insufficient.

At Skaraz Data, we build the geospatial data pipelines and risk analytics that connect satellite observations to insurance decision-making. From SAR flood footprint processing to portfolio exposure dashboards, we help insurers turn raw Earth observation data into actionable risk intelligence. If your team is evaluating how to integrate satellite flood data into your workflow, let’s talk.