Europe’s deadliest wildfire season in a decade. Record drought losses across the American Midwest. A cyclone season in the Arctic that caught shipping insurers off guard. The common thread behind each of these events is not just climate change. It is the growing gap between the data insurers use to price risk and the data that actually describes what the atmosphere is doing.

That gap is closing, and the catalyst is reanalysis data. Specifically, datasets like ECMWF’s ERA5 are quietly becoming the backbone of a new generation of climate risk products. If you work in insurance, catastrophe modeling, or ESG risk scoring, this shift will reshape how you build, price, and validate your models over the next three to five years.

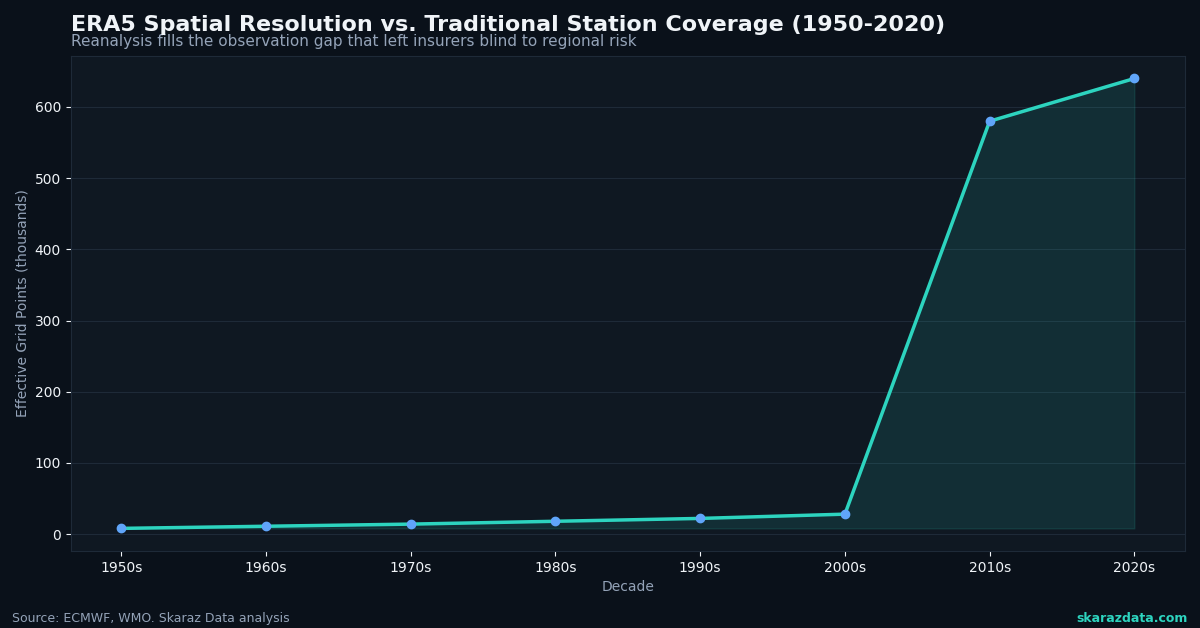

What Reanalysis Data Actually Is (and Why It Matters Now)

Reanalysis datasets combine historical weather observations (station data, satellite readings, radiosondes) with numerical weather prediction models to produce a physically consistent, gap-free record of the atmosphere. ERA5, the current gold standard from ECMWF, delivers hourly data on a 31 km global grid going back to 1940, with over 200 atmospheric, land, and ocean variables.

For insurance and risk applications, this solves three problems at once:

- Consistency over time. Station networks change, instruments get upgraded, coverage shifts. Reanalysis corrects for these inhomogeneities, giving you a stable baseline for trend detection.

- Global coverage without gaps. You can assess wind, precipitation, and temperature hazards in regions with sparse observational networks, from sub-Saharan West Africa to Arctic shipping corridors.

- Hourly temporal resolution. This matters for peril modeling. A daily average temperature does not capture the three-hour heatwave spike that triggers crop stress or the six-hour wind burst that causes structural damage.

A recent Nature study on renewable energy yield assessment confirmed what risk modelers have suspected: gridded reanalysis products consistently outperform raw station data for spatial hazard estimation, particularly in areas with complex terrain or limited ground truth.

Four Ways ERA5 Is Already Inside Insurance Products

1. Parametric Insurance Triggers

Parametric products pay out when a measurable index crosses a threshold, not when a loss adjuster files a report. ERA5 provides the historical baseline to calibrate those triggers. For drought parametrics in agriculture, teams are combining ERA5 soil moisture and precipitation fields with satellite vegetation indices to build payout curves. A new near-global agro-climatological drought monitoring dataset published in Nature’s Scientific Data uses exactly this approach, fusing reanalysis with remote sensing to track drought onset across +150 countries.

2. Catastrophe Model Calibration

Traditional cat models rely on event sets, synthetic catalogs of storms, floods, and quakes. ERA5’s 80+ year hourly record gives modelers a much richer event library to validate against. The recently published ERA5-based global wildfire danger dataset, built on the Canadian Fire Weather Index system, is a perfect example: it translates raw reanalysis fields into operationally relevant fire risk metrics that cat model vendors can ingest directly.

3. Underwriting Enrichment at the Grid Cell Level

When an underwriter evaluates a commercial property portfolio spread across 12 countries, they need consistent hazard metrics everywhere. ERA5 delivers wind gust return periods, extreme precipitation frequencies, and heat stress indices on the same grid, same methodology, everywhere on Earth. The European Extreme Events Climate Index (E3CI), built on reanalysis and satellite data, demonstrates how these consistent grids translate into actionable hazard monitoring for weather-induced perils across an entire continent.

4. Climate Change Signal Detection

Insurers need to answer a deceptively simple question: is the risk getting worse, and by how much? Reanalysis lets you compute robust trend statistics because the data is physically consistent across decades. A recent reassessment of mean and extreme climates over West Africa showed that reanalysis products can reliably detect shifting precipitation patterns and temperature extremes, even in regions where observational networks have deteriorated over time.

The Operationalization Challenge

Having good data is necessary but not sufficient. As a recent RealClimate analysis argues, there is a pressing need to move climate science from research mode into operational mode. For insurance applications, that means:

- Pipeline engineering, not just analysis. ERA5 updates daily with a five-day lag. Building a production pipeline that ingests, processes, and serves terabytes of gridded data requires serious data engineering, not just a Jupyter notebook.

- Spatial downscaling. A 31 km grid cell is too coarse for property-level risk. You need statistical or dynamical downscaling, bias correction, and validation against local observations. This is where most projects stall.

- Peril-specific feature engineering. Raw atmospheric variables (temperature, wind speed, precipitation) need to be transformed into insurance-relevant metrics: return periods, severity curves, compound event indices. Each peril has its own physics and its own modeling quirks.

- Regulatory and audit trail requirements. Solvency II and IFRS 17 demand that insurers can explain and reproduce their risk estimates. Black-box ML on raw reanalysis fields will not pass muster. You need transparent, well-documented transformation pipelines.

The Copernicus Climate Change Service (C3S) is pushing hard on this operationalization front. Their recent work supporting the finance and insurance sectors explicitly targets the gap between raw climate data and decision-ready risk metrics.

What This Means for Your Climate Risk Strategy

If you are building or buying climate risk analytics, here is the practical takeaway:

- Demand reanalysis-based baselines. Any vendor showing you climate risk scores without disclosing their reference dataset is selling you a black box. ERA5 (or its successors) should be the minimum standard for historical hazard characterization.

- Invest in the pipeline, not just the model. The competitive advantage in climate risk is increasingly about data engineering: ingestion, quality control, spatial processing, and serving infrastructure. The science is largely settled. The engineering is not.

- Think in compound events. Single-peril analysis is becoming obsolete. The real losses come from drought plus heat, or wind plus flood. Reanalysis datasets give you the multivariate, temporally consistent fields needed to model these compound risks properly.

- Plan for updates. ERA5 is not static. ERA6 is in development. Your architecture needs to handle dataset version transitions without breaking downstream products.

The insurance industry spent decades pricing climate risk with sparse, inconsistent, and spatially biased data. Reanalysis changes that equation fundamentally. The organizations that build robust pipelines from gridded climate data to actuarial-grade risk metrics will define the next era of climate-aware underwriting.

At Skaraz Data, we build exactly these pipelines: from raw ERA5 and satellite data through to production-grade climate risk indicators tailored for insurance, agriculture, and ESG applications. If your team is navigating the shift from traditional loss data to climate-forward risk modeling, let’s connect.